Newsletter Subscribe

Enter your email address below and subscribe to our newsletter

Enter your email address below and subscribe to our newsletter

Picture this: You’re sitting in your favorite armchair, ready to buy a delightful set of copper-bottomed pans from a website you found on Facebook. You reach into your physical wallet and pull out two shiny pieces of plastic. One says “Debit.” The other says “Credit.”

To the untrained eye, they look identical. They both have 16 numbers, an expiration date, and a security code that practically requires an electron microscope to read. But in the wild, unpredictable jungle of the internet, these two cards are as different as a heavily armored tank and a golf cart made of cheese.

If you’ve ever wondered which card is actually safe to use online, you are not alone. It’s one of the most common questions we get, right up there with “Why does my printer hate me?” Today, we’re going to look at why using one of these cards is a breeze, while using the other online could turn your bank account into a hacker’s personal piggy bank.

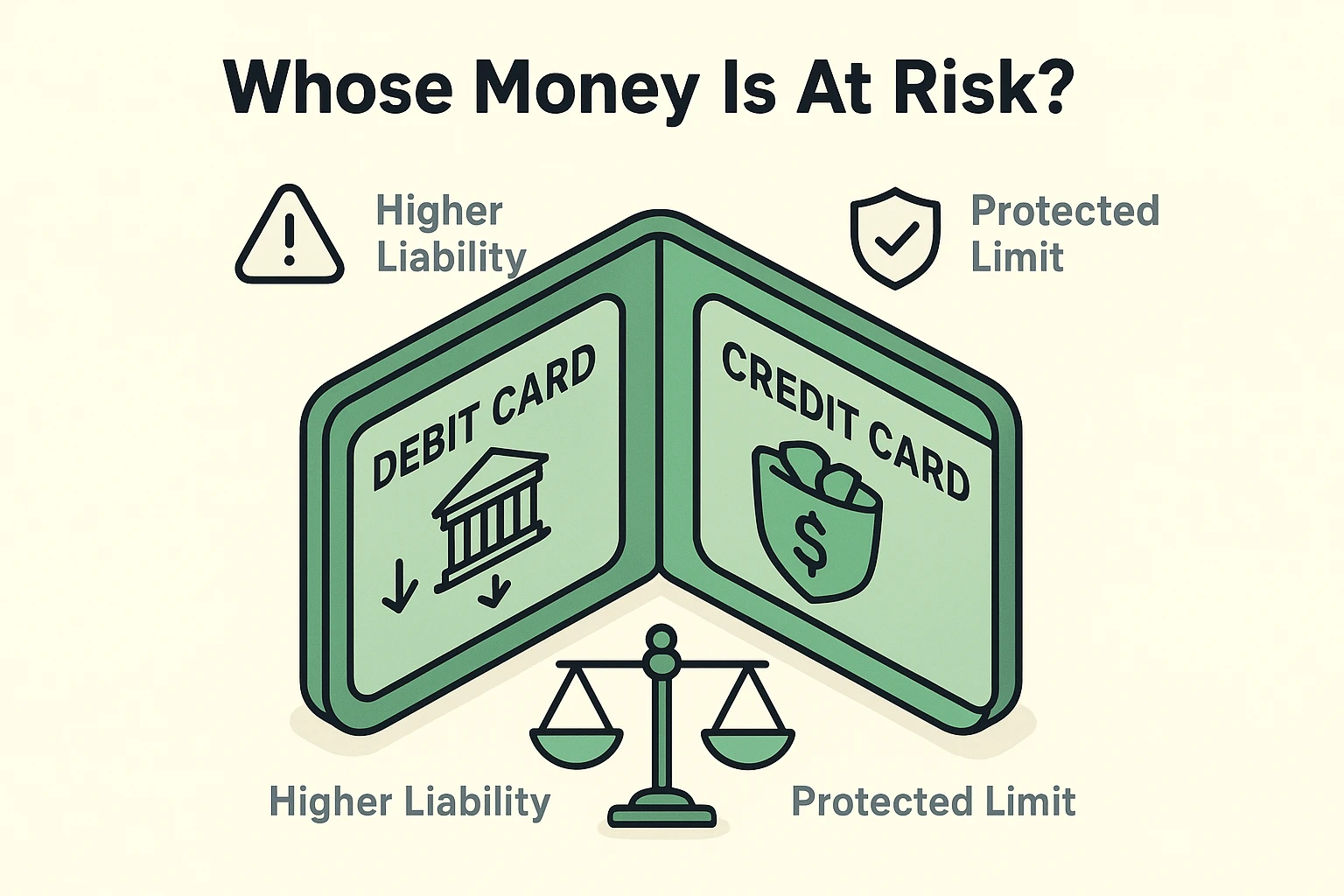

Think of your personal bank account as a giant bucket of water. This bucket holds your life savings, your mortgage money, and the funds you need to buy groceries this week.

A debit card is like sticking a giant drinking straw directly into that bucket. If a scammer gets hold of your debit card number, they can suck the bucket dry before you’ve even finished your morning coffee. This leads to what we call the “Domino Effect,” where suddenly your mortgage payment bounces, your electric bill is late, and you’re racking up overdraft fees like they’re going out of style.

A credit card, on the other hand, is a completely separate, smaller bucket of water that belongs entirely to the bank. If a scammer steals from it, they are stealing the bank’s money, not yours. Your personal bucket remains untouched and perfectly safe.

When it comes to legal liability, the government treats these two buckets very differently. Thanks to the Fair Credit Billing Act (FCBA), your liability for credit card fraud maxes out at $50, and most banks will even waive that. But with a debit card, if you don’t report the fraud fast enough, the Electronic Fund Transfer Act says you could potentially lose every single penny in the account.

So, we know credit cards are legally safer. But what if we told you there’s a way to make them even more secure? Enter the digital wallet, like Apple Pay or Google Pay on your smartphone.

Now, I know what you’re thinking: “I barely trust my physical wallet not to get lost in the couch cushions, why would I trust my phone with my money?” It’s a completely fair question. But setting up a digital wallet isn’t just a gimmick for millennials; it’s the absolute gold standard of digital self-defense.

When you use a digital wallet, it uses a fancy security feature called “tokenization.” Let’s ditch the tech jargon, though. Imagine giving a cashier a single-use, temporary key that opens a lockbox with exactly the right amount of money for that one purchase, and then the key immediately evaporates into thin air.

Even if a hacker breaks into that store’s computer systems months later, all they’ll find is a pile of useless, evaporated digital keys. Your actual credit card number was never handed over, so it remains completely hidden and safe.

Now we must venture into the treacherous waters of Peer-to-Peer (P2P) payment apps. These are apps like Venmo, Cash App, and Zelle. They are fantastic for splitting a dinner bill with your friends or sending your grandson a quick $20 for mowing the lawn.

But using them to buy goods from strangers online? That’s exactly like handing an envelope of untraceable cash to a guy in a dark alley who promised to mail you a toaster. Once you hit “send,” that money is gone, and getting it back is about as likely as winning the lottery twice on a Tuesday.

This is where we need to explain the crucial difference between a “Fraud” and a “Scam.” Fraud is when someone steals your card and buys a television without your permission—the bank will usually step in and refund this. A scam, however, is when someone tricks you into hitting the “send” button yourself.

Because you technically authorized the transaction, the bank will often just shrug and say, “Sorry, you pressed the button.” P2P apps offer virtually zero buyer protection, so they should strictly be used with people you personally know and trust.

Let’s say the worst happens. You notice a charge you didn’t make, or you realize the “customer service rep” you just sent money to was actually a scammer. Don’t panic, but don’t take a nap, either. You are now in the “Golden Hour” of fraud recovery.

Step one: Call your bank or credit card company immediately using the phone number printed on the back of your physical card. Do not search for the phone number on Google, as scammers often create fake customer service pages just waiting for panicked people to call them.

Step two: Lock your card. Most banking apps now have a simple toggle switch that lets you freeze the card instantly. This stops the bleeding while you figure out exactly what happened.

Step three: Make sure your digital doors are locked tight. This is the perfect time to ensure you have strong auth enabled on all your financial apps, which requires a second step beyond just your password to log in.

We strongly advise against it. If you absolutely must, only use it on highly trusted, secure websites like your local utility company. But even then, using a credit card is vastly safer for your peace of mind.

That is a very wise concern! A great workaround is to get a credit card, use it only for online purchases, and pay the balance off in full every single week. You get the heavy-duty security shield without paying a single dime in interest charges.

PayPal is generally safe if you use the “Goods and Services” option during checkout. If a seller ever asks you to use the “Friends and Family” option to avoid paying a fee, run away! That immediately strips away all your buyer protections.

Navigating the internet doesn’t have to feel like walking through a digital minefield in clown shoes. By making a few simple tweaks to how you pay, you can shop, browse, and manage your money with absolute confidence.

Remember our golden rule: Keep your debit card tucked safely away for ATM visits, and let your credit card do the heavy lifting online. You might also be seeing new options from your bank and wondering about setting up a paze account to simplify checkouts, which is just another great step toward keeping your real card numbers hidden from prying eyes.

Stay curious, stay cautious, and don’t let the scammers win. Your life savings took a long time to build; let’s keep it exactly where it belongs!