Newsletter Subscribe

Enter your email address below and subscribe to our newsletter

Enter your email address below and subscribe to our newsletter

Picture this: You’re just settling in for the evening. You’ve got a warm cup of tea, your favorite fuzzy slippers are on, and Alex Trebek’s successor is about to read the first Jeopardy! clue. Suddenly, the phone rings. “Caller ID says ‘Chase Bank’.”

You answer, and a very stern-sounding person tells you that a hacker in a distant, unpronounceable country just bought 14 flat-screen TVs using your credit card. Your heart rate spikes to hummingbird levels. Your tea gets cold. You are officially in a state of sheer panic, ready to do whatever this mysterious voice says to save your hard-earned retirement funds.

If you’ve experienced this terrifying jolt of adrenaline, you are definitely not alone. Scammers know that the fastest way to bypass your common sense is to hit the “panic” button. We call this the “Panic Barrier.” Once you’re panicking, you stop asking logical questions. But today, we’re going to give you the exact tools to tell the difference between a real bank employee and a crook trying to steal your cookie money.

Here is a secret that the major banks want you to know: real bank fraud departments are incredibly boring. I mean, wonderfully, gloriously boring. They are strictly process-driven and have no interest in your adrenaline levels.

A scammer’s script is built entirely on high urgency. They will use phrases like “immediate action required,” “arrest warrant,” or “your account will be frozen in ten minutes.” They want you moving so fast you trip over your own slippers.

A real bank employee, on the other hand, sounds like they are reading the phone book. They have usually already frozen the suspicious transaction before they even called you. They don’t need you to panic; they just need a simple “yes” or “no” from you on whether you actually tried to buy a yacht in Sweden this morning.

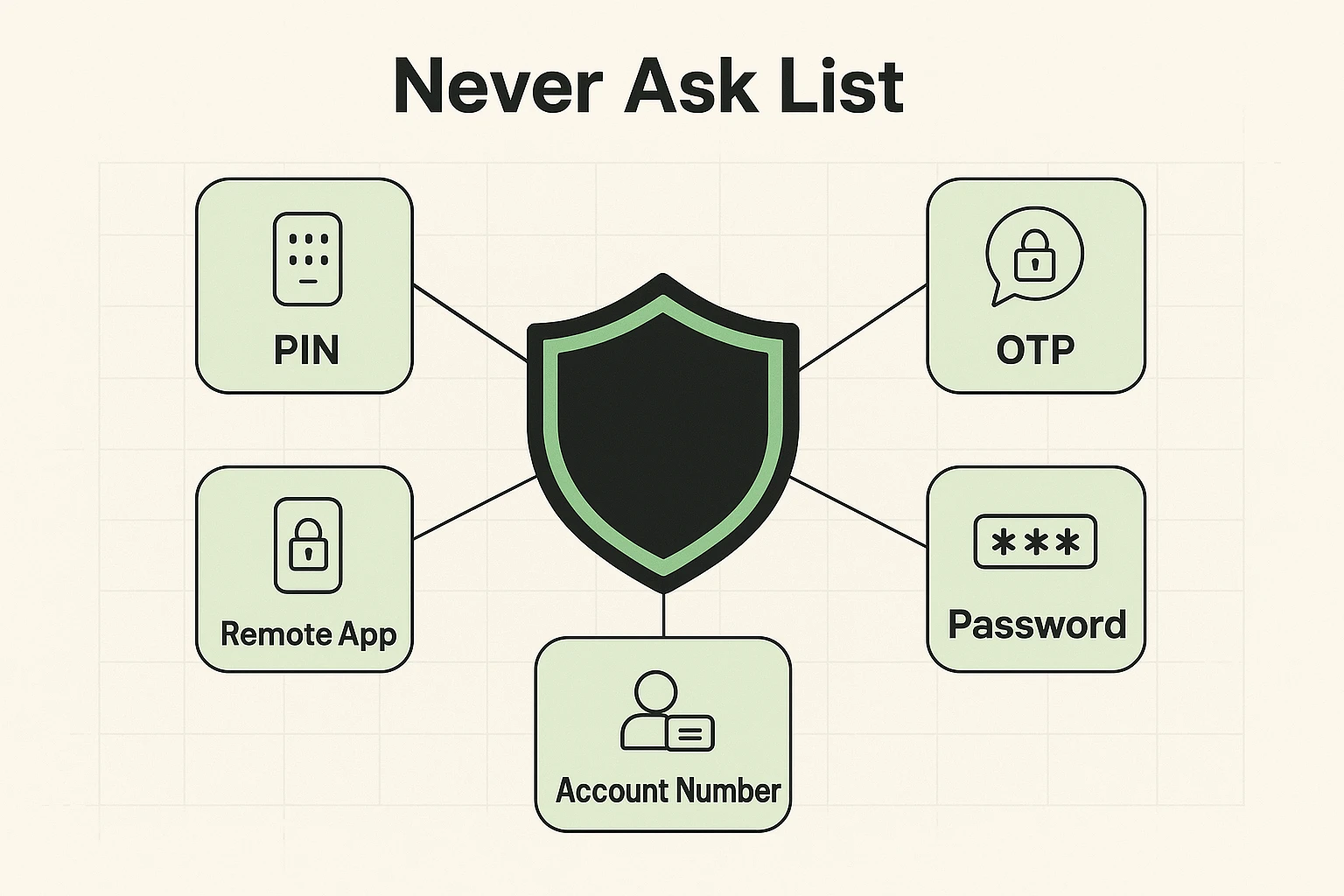

Let’s establish a baseline of things banks will never ask you for. Think of this as your digital armor. Whether it’s a phone call, a text message, or an email, a legitimate financial institution will never request these items.

So, how do you verify if the caller is real? The advice you’ve probably heard a million times is: “Hang up and call the number on the back of your card.” And that is absolutely the right move! But there is a tiny, sneaky catch you need to know about.

In some phone systems (especially landlines), scammers use a trick called “line trapping.” Here’s how it works: you hang up the phone, but the scammer doesn’t. The line actually stays open.

When you pick the phone right back up to dial your bank, you just hear a fake dial tone played by the scammer. You dial the number on your card, the scammer’s “supervisor” answers, and you think you’re talking to the real bank. Talk about devious!

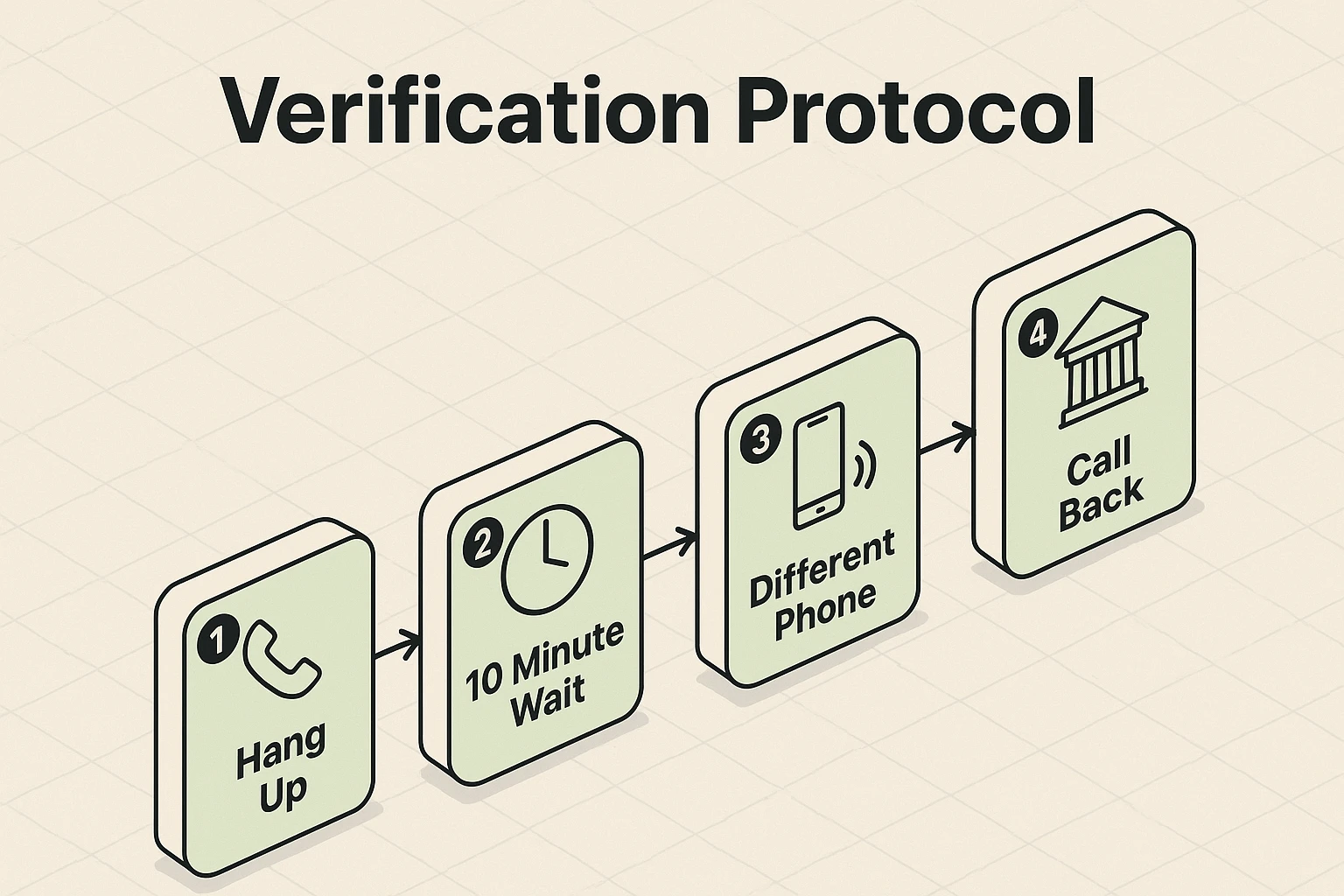

The Fix: If you get a suspicious call on your landline, hang up and wait at least 10 full minutes before picking it up again to ensure the line has fully cleared. Better yet, use a completely different phone (like your cell phone) to call the number on the back of your card.

To make your digital life safer, there are a few modern tools that sound complicated but are actually quite simple to use. One is a Virtual Credit Card. Some banks let you generate a temporary card number for online shopping. If a scammer steals it, they get nothing but a canceled number.

Another great tool is App-based verification. Instead of getting a text message that can be easily faked or intercepted, the bank sends an alert straight to their official app on your smartphone. You just log in with your fingerprint or face, and tap “Yes, that was me” or “No, it wasn’t.”

Of course, relying on your smartphone for security brings up a new worry: what if you drop your phone in a lake? If you rely on these security codes and misplace your device, you might want to read up on how to handle your two factor authentication lost phone scenario so you don’t accidentally lock yourself out of your own life.

If you’re still worried about clicking the wrong link in a text message, there’s artificial intelligence for that now, too. You can use tools like a bitdefender scam detector to safely check suspicious messages before you ever interact with them.

Generally, yes. Scammers usually need you to type in your password or personal info on their fake website. However, clicking the link might confirm to them that your phone number is active. Close the window immediately, and never type your details into a link you clicked from a random text.

They didn’t. Scammers use a trick called “caller ID spoofing” to make their number look like it’s coming from your town, or even spoof it to say your actual bank’s name. Never trust Caller ID; it’s easier to fake than a toupee in a windstorm.

Absolutely not! Real bank employees are trained to expect this. If you hang up and call the official number on the back of your card, the bank will actually be thrilled that you are practicing good security.

The next time your phone rings and a frantic voice tells you your account is compromised, remember the 3-Second Rule. Take a breath. Look for the panic tactics. Remember that real banks are boring, process-driven, and already have your account information.

As a practical step today, take a sticky note and write “HANG UP, WAIT 10 MIN, CALL NUMBER ON CARD” and stick it next to your home phone or on your fridge. This creates a physical reminder that breaks the digital Panic Barrier before it even starts.

You are in control. By keeping a cool head and refusing to be rushed, you can safely navigate the digital world—and get right back to watching Jeopardy! in peace.