Newsletter Subscribe

Enter your email address below and subscribe to our newsletter

Enter your email address below and subscribe to our newsletter

Imagine you’re relaxing in your favorite armchair, enjoying a cup of coffee and watching a rerun of Columbo. Suddenly, the phone rings. It’s a very official-sounding person named “Steve” from an unpronounceable department, kindly informing you that you’ve just purchased a fleet of Jet Skis in a landlocked state. You don’t even like water, let alone motorized watercraft that require a helmet.

Welcome to the modern age of identity theft, where scammers are working overtime to buy ridiculous things with your good name. Fortunately, you have two powerful tools to stop them: the fraud alert and the credit freeze. But figuring out which one to use can feel like trying to program a VCR in the dark.

Let’s clear up the confusion so you can protect your hard-earned credit without losing your mind.

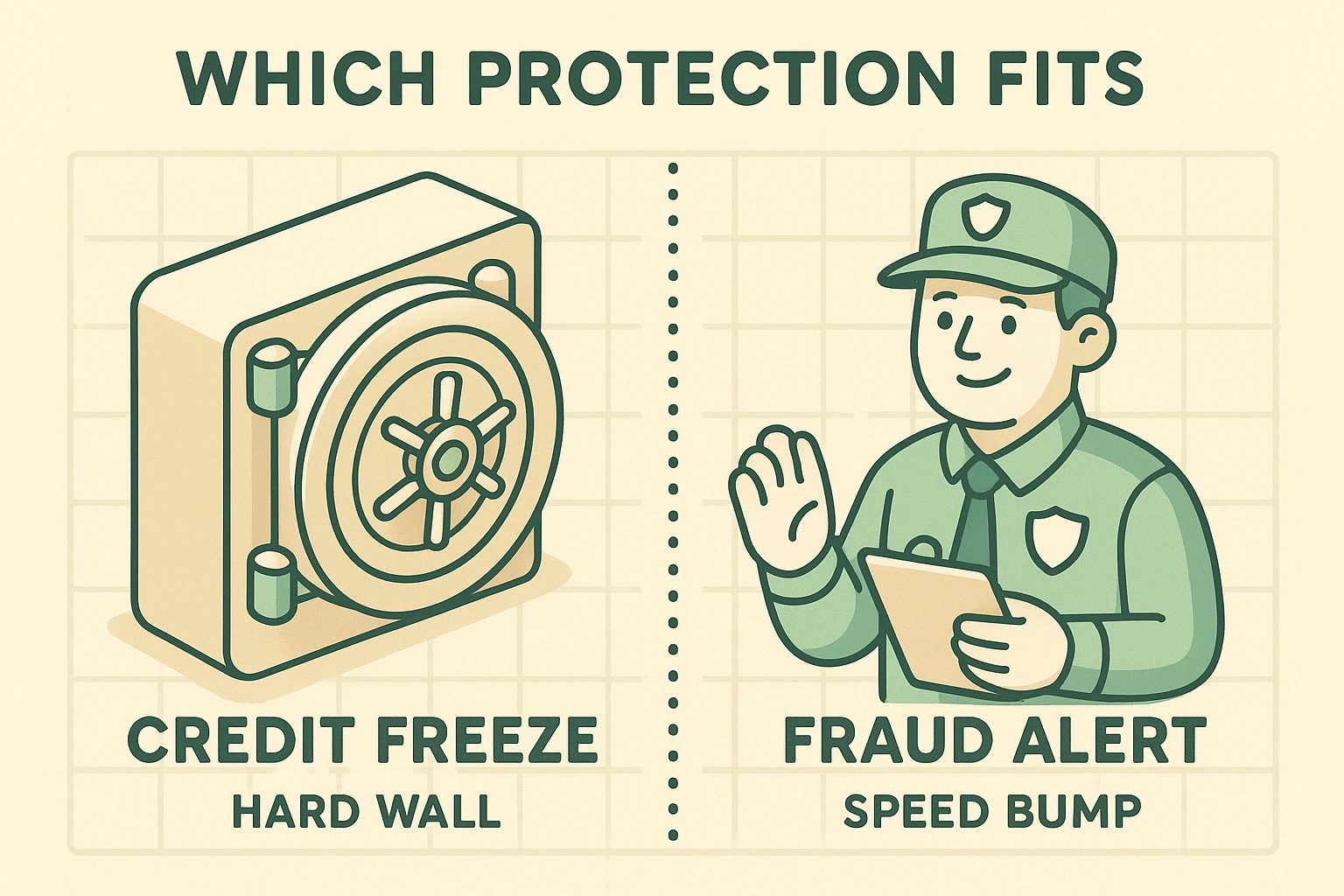

To understand the difference between a fraud alert and a credit freeze, think of your credit report as a very exclusive nightclub.

A fraud alert is like hiring a security guard to stand outside the club with a clipboard. When someone tries to open a new credit card in your name, the guard says, “Hold on, let me call the boss (you) to make sure this is legit.” It’s a helpful speed bump that slows the bad guys down. But if the guard gets distracted, or the scammer is particularly slick, someone might still sneak in.

A credit freeze, on the other hand, is like sealing the nightclub behind a ten-ton steel bank vault door. Nobody gets in or out. If a scammer tries to open an account, the bank is denied access to your credit report entirely, and the application is instantly rejected. It is a hard wall that stops identity thieves in their tracks.

Before we go any further, let’s address the elephant in the room—or rather, the salesperson in the room. If you visit the websites for the “Big 3” credit bureaus (Equifax, Experian, and TransUnion), you’ll likely see them pushing something called a “Credit Lock.”

They will make it sound incredibly convenient, like a magical app on your phone that solves all your problems. Here is the catch: they usually want you to pay a monthly fee for this “service.” They are essentially selling you a shiny, branded version of something you already own.

A credit freeze is your legally guaranteed right, and it is 100% free. By federal law, these companies cannot charge you a single penny to freeze or unfreeze your credit. So, skip the fancy, paid “lock” and go straight for the free, federally protected “freeze.”

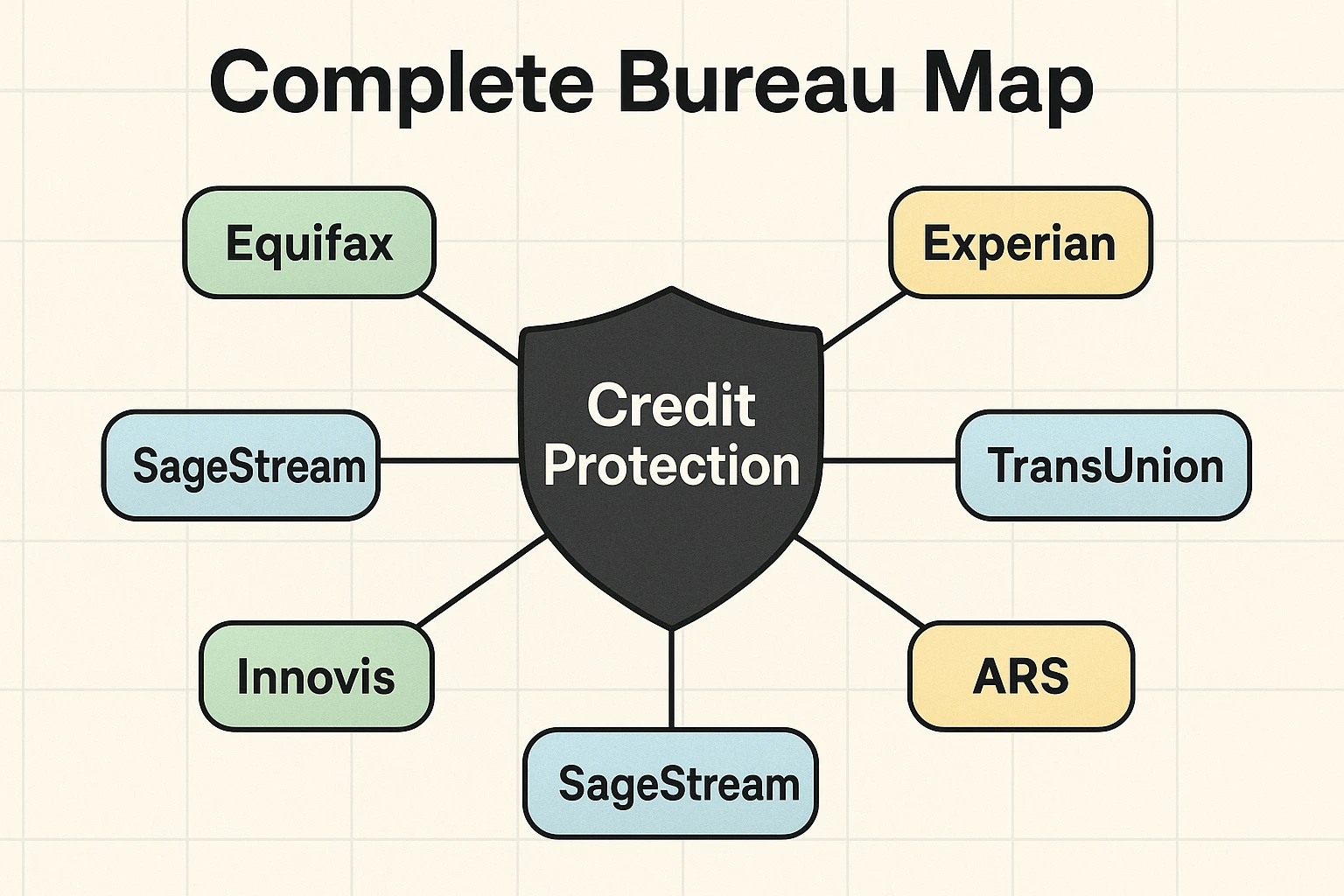

Most people know about the Big 3: Equifax, Experian, and TransUnion. Freezing your credit with them is a fantastic first step. It’s like locking the front, back, and side doors of your house.

But what about the basement windows? Scammers are sneaky, and when they realize the main doors are locked, they try to open retail store credit cards or get cell phone financing. These companies often check your credit using smaller, lesser-known bureaus that you’ve probably never heard of.

To get “full armor” protection, you also need to freeze your files at secondary bureaus like Innovis, ARS (Advanced Resolution Services), and SageStream (now part of LexisNexis). It takes a few extra minutes, but it stops scammers from buying 80-inch televisions on a big-box store card in your name.

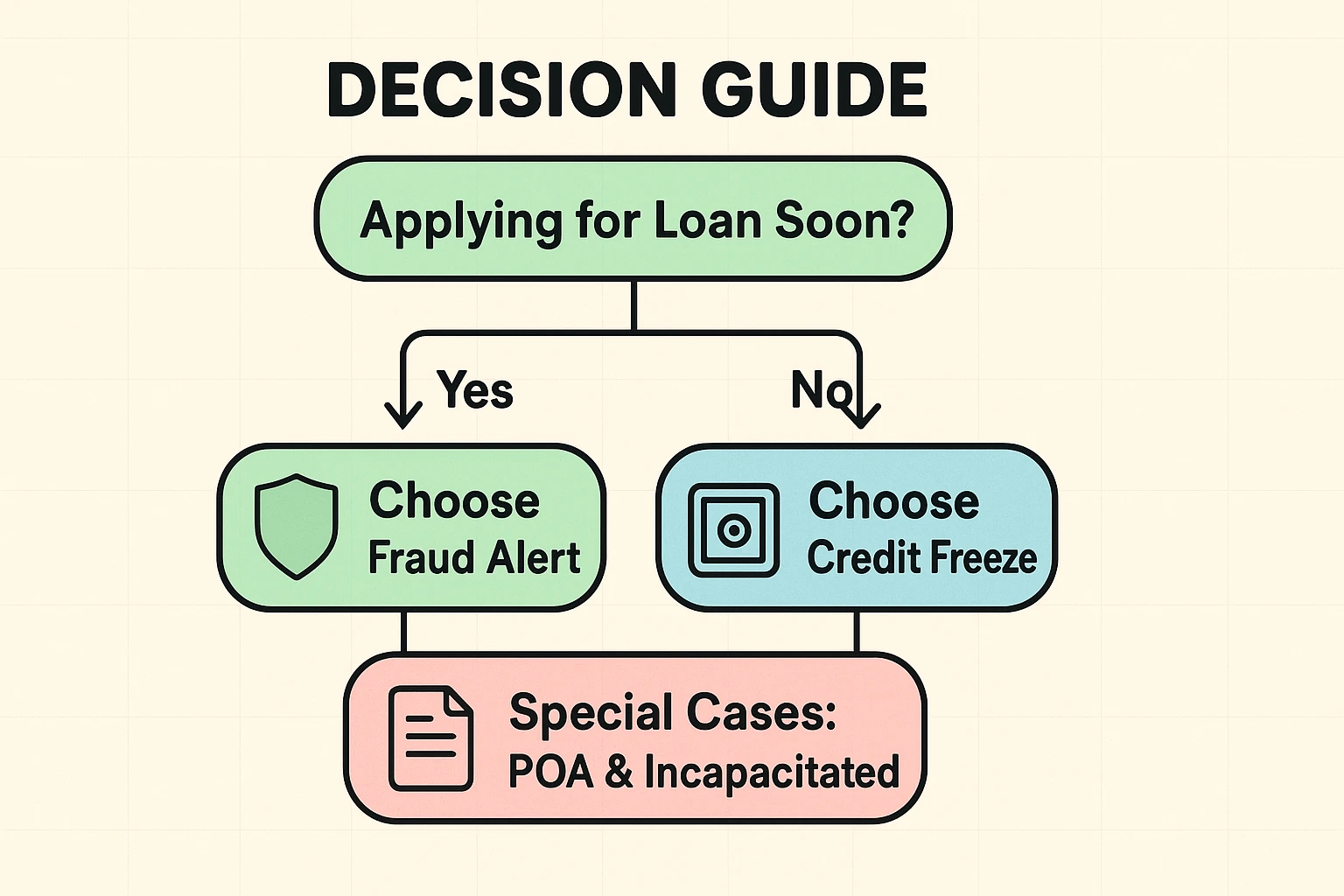

Sometimes you aren’t just managing your own credit; you might be taking care of a spouse or an aging parent. If you have Power of Attorney (POA) for someone, or if you are managing affairs for an incapacitated adult, you can (and absolutely should) freeze their credit, too.

Unfortunately, you can’t usually do this online with a simple click. You’ll need to use the old-fashioned physical mail-in option, which requires a bit of patience and a printer.

The bureaus require specific “Incapacitated Adult” forms and copies of your legal POA documents. It involves a bit of paperwork and a trip to the post office, but securing a vulnerable loved one’s identity is well worth the price of a few postage stamps.

A common worry is that a credit freeze will trap you if you suddenly need to buy a car or apply for a new apartment. Don’t panic! You have the power of the “Emergency Thaw.”

When you freeze your credit, the bureaus will give you a special PIN or ask you to create an online account. Keep this information very safe—perhaps in a printable “PIN Wallet” stored entirely offline in your actual, physical filing cabinet.

If you are sitting at the car dealership, you can simply log into the bureau’s website on your smartphone, enter your PIN, and temporarily “thaw” your credit for a few days. Once the loan goes through, the vault door automatically locks itself again. It’s safe, free, and puts you entirely in control.

Not even a little bit. A freeze only stops new accounts from being opened. Your current credit cards will still work, and your score will continue to go up (or down) based entirely on your normal payment history.

Actually, no! If you place a fraud alert with just one of the Big 3 (like Experian), they are legally required by the government to notify the other two. But remember, a credit freeze is different—that requires you to contact each bureau individually.

A standard fraud alert lasts for exactly one year. You can renew it, but you have to remember to do it yourself. A credit freeze lasts until you actively decide to take it off, making it a much better “set it and forget it” option for your peace of mind.

Deciding between a fraud alert and a credit freeze really comes down to your current situation. If you are actively shopping for a mortgage or a new car this month, a fraud alert might be the easiest short-term speed bump to use while lenders are checking your history.

But for the vast majority of us who aren’t applying for new loans every week, the credit freeze is the undisputed heavyweight champion of identity protection. It’s free, it’s strong, and it gives you ultimate control over your financial vault.

Take an hour this week to visit the official websites for Equifax, Experian, TransUnion, and the secondary bureaus. Your future self—who thankfully does not own a fraudulent fleet of Jet Skis—will thank you!