Newsletter Subscribe

Enter your email address below and subscribe to our newsletter

Enter your email address below and subscribe to our newsletter

Remember the good old days of scams? Back when a foreign prince would politely email you, offering thirty squillion dollars in exchange for your checking account number? You’d have a good laugh, hit delete, and go about your day feeling like a cybersecurity genius. Oh, how times have changed.

Today’s scammers don’t write in broken English, and they certainly don’t claim to be royalty. Instead, they wear sharp digital suits, masquerade as financial gurus, and build fake investment platforms that look more professional than your actual bank’s website. It’s enough to make you want to stuff your life savings inside your mattress, right next to your collection of slightly expired coupons.

But before you start ripping the stuffing out of your Sealy Posturepedic, let’s get one thing straight: Scammers don’t target you because you’re gullible or out of touch. They target you because you are an elite target. You’ve spent a lifetime working, saving, and building wealth, which is exactly what they want. You aren’t vulnerable; you’re valuable.

We’ve all heard the phrase, “If it sounds too good to be true, it probably is.” But in the digital age, we need to upgrade that advice. Let’s talk about the “Risk-Reward Mirror.” In the real world of investing, risk and reward sit on opposite sides of a seesaw.

If someone promises you a “guaranteed” return of 20% in a world where regular savings accounts are paying peanuts, that seesaw is broken. “Guaranteed” and “High Return” simply cannot exist in the same sentence unless you’re reading a fairy tale. Real investments fluctuate, and legitimate financial advisors are legally required to tell you about the risks.

Scammers, on the other hand, love the word “guaranteed.” They also love urgency and secrecy. If a new digital friend tells you about a “can’t-miss” opportunity but insists you must act right now and keep it a secret from your family, your internal alarm bells should be ringing loud enough to wake the neighbors.

So, how do we spot these digital pickpockets? It starts with how they contact you. A legitimate broker is never going to casually message you on WhatsApp or LinkedIn with a tip on the next big cryptocurrency. If you get an unsolicited message offering financial advice, treat it like an uninvited raccoon in your garage: back away slowly and lock the door.

Just like you might research techniques for stopping a wangiri fraud attack when your phone rings once from a bizarre international number, you need a firm strategy for ignoring random investment pitches. Engaging with them, even to say “no thank you,” just tells the scammer your number is active.

Another major red flag is the payment method. If your new “broker” asks you to fund your investment using cryptocurrency, wire transfers, or—heaven forbid—gift cards, slam the brakes. Legitimate investment firms do not ask you to buy gold bars or Bitcoin to open a retirement account.

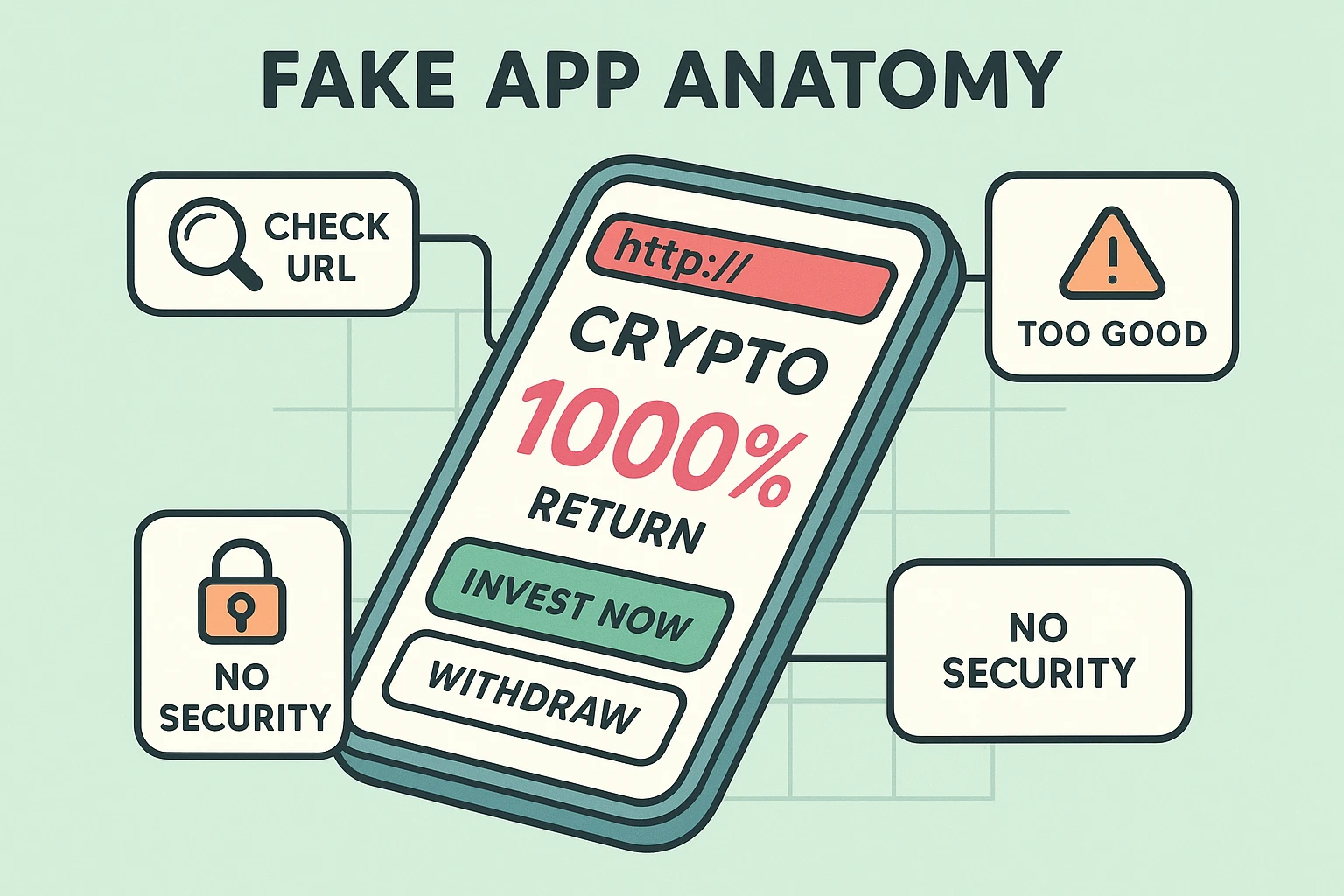

Here is a common misconception: If an investment app is available in the Apple App Store or Google Play Store, it must be safe and vetted, right? Sadly, no. Scammers are incredibly good at slipping “cloned apps” past the security guards.

These fake apps look identical to legitimate trading platforms. They’ll show you beautiful charts and growing account balances, but the numbers are entirely made up. Before you download any financial app, take a moment to independently check their website on a standard web browser to ensure the app is actually connected to a real company.

I know, “Pig Butchering” sounds like a terrible, messy name for a barbecue joint. Unfortunately, it’s actually the name of the most devastating financial scam of our current era. Unlike the smash-and-grab scams of the past, this is a psychological long game.

It usually starts with a “wrong number” text message. You might get a text saying, “Hi Jim, are we still on for golf tomorrow?” You politely reply, “Sorry, you have the wrong number.” Instead of apologizing and leaving, the scammer says, “Oh, you seem so nice! Let’s be friends.” Over the next few months, they groom you, chatting about life, family, and eventually, their amazing success trading cryptocurrency.

Once you trust them, they introduce you to “Phantom Wealth.” They might convince you to invest just $100 on their fake platform. A week later, they let you withdraw $150. You think, “Wow, this is real!” By letting you win a little bit, they butcher your skepticism, paving the way to steal your entire life savings when you decide to go all in.

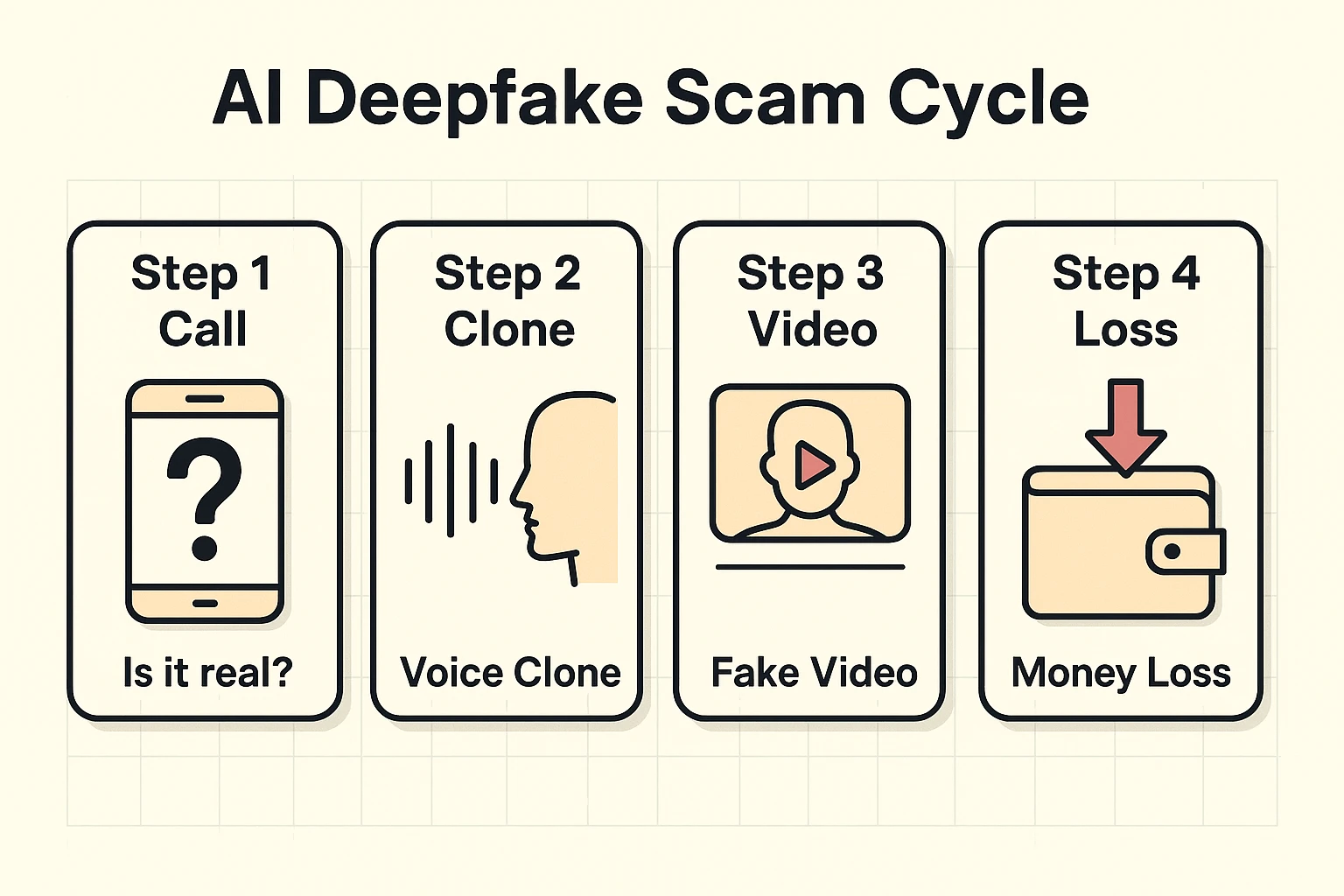

If fake apps and long-con text messages weren’t enough, we now have to deal with Artificial Intelligence. Scammers only need a few seconds of audio—often pulled right from a social media video—to clone a voice perfectly.

This means you could receive a phone call that sounds exactly like your grandson, begging for bail money, or a video that looks identically like a famous billionaire endorsing a new crypto coin. It’s terrifying, but you aren’t powerless. If you ever get a strange call from a loved one asking for money, hang up and call them right back on the number you already have saved in your phone.

To give yourself an extra layer of protection online, you might consider utilizing a tool like a bitdefender scam detector. These tools can act as an artificial intelligence guard dog, helping you sniff out fraudulent links and deepfake scams before they bite.

The goal here isn’t to make you terrified of technology; it’s to turn you into a digital private investigator. From now on, you are the auditor of your own wealth. Your greatest weapon against scammers isn’t a complex software program—it’s time.

Scammers use urgency because they know that if you stop to think, their entire illusion falls apart. Implement the “24-Hour Rule” for your finances. No matter how amazing an investment sounds, or how panicked a caller seems, simply say, “I never make financial decisions on the spot. I’ll review this tomorrow.”

Take those 24 hours to talk to a trusted family member, call your real bank, or check the SEC’s BrokerCheck tool to verify licenses. A legitimate investment will still be there tomorrow. A scammer will disappear into the digital ether the moment they realize they’re dealing with an informed auditor.

A crypto wallet is basically a digital bank account that holds cryptocurrency instead of standard money. If an online friend or a stranger on the phone tells you to open one to make an investment, stop immediately. It’s almost certainly a scam.

Unfortunately, money sent via crypto or wire transfer is very difficult to recover. Beware of “Recovery Scams”—these are scammers who contact you after you’ve been robbed, promising to get your money back for an “upfront fee.” They are just trying to steal from you twice.

In the United States, you should report investment fraud to the SEC, the FBI’s Internet Crime Complaint Center (IC3.gov), and your local authorities. Even if they can’t get your money back, your report helps them track down the networks running these operations.

Navigating the digital financial world doesn’t have to feel like walking barefoot through a room full of Legos. Armed with a healthy dose of skepticism and a clear understanding of modern tactics, you can confidently protect your hard-earned nest egg. Stay curious, stay cautious, and never let anyone rush your wallet.