Newsletter Subscribe

Enter your email address below and subscribe to our newsletter

Enter your email address below and subscribe to our newsletter

Picture this: You’re sorting through your afternoon mail, expecting nothing more thrilling than a flyer for half-price gutter cleaning. Instead, you open a letter congratulating you on the purchase of a brand-new, neon-green jet ski in Miami. The only problem? You live in Ohio, and your most extreme water sport involves a slightly overfilled bathtub.

Welcome to the incredibly frustrating, entirely un-fun club of identity theft victims. If this sounds familiar, take a deep breath. You are far from alone in this mess. Finding out someone has opened fraudulent accounts in your name feels like being assigned a part-time job you never applied for, with a boss who speaks exclusively in legal jargon.

Most guides out there simply tell you to “report it online” and wish you good luck, leaving you to fight a maze of automated phone trees. Today, we are going to skip the fluff. We’ll show you exactly how to build an ironclad case, fight back against stubborn credit bureaus, and reclaim your good name—without needing a law degree.

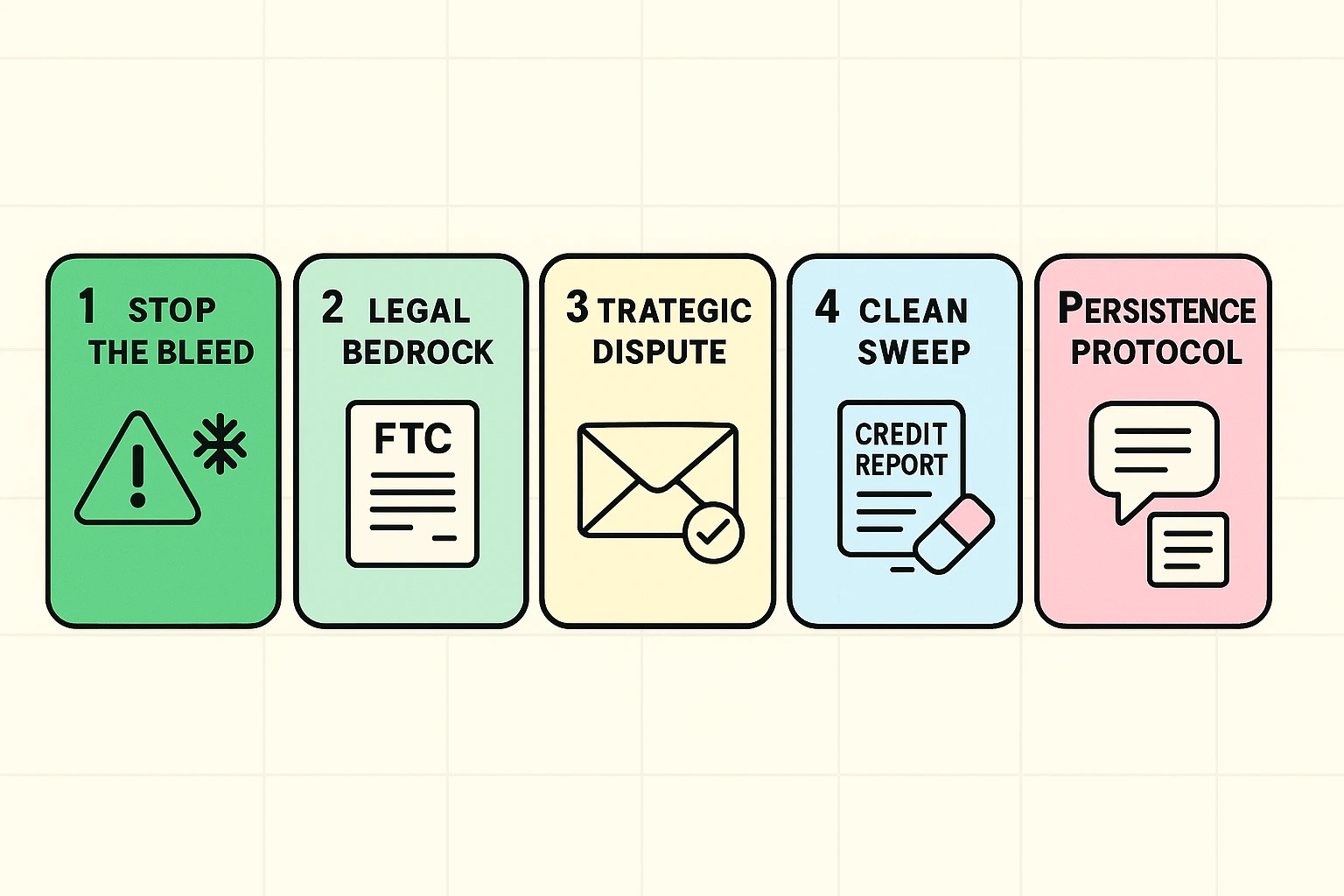

When you first discover fraud, your brain might urge you to panic. Tell your brain we don’t have time for that right now. Your immediate goal is to “stop the bleed” so the scammers can’t do any more damage.

First, contact the fraud department of the company where the bogus account was opened and tell them to freeze it immediately. Next, contact one of the three major credit bureaus (Experian, Equifax, or TransUnion) to place a free fraud alert on your file. Once you notify one, they are legally required to tell the other two, saving you from repeating your story three times.

This is also the perfect time to secure your legitimate accounts so the scammers don’t pivot. Change your passwords to something complex, and be sure to set up strong auth—also known as two-factor authentication—wherever possible. It acts like a digital deadbolt on your front door, keeping the riff-raff out even if they guess your password.

Here is a secret that the big financial institutions don’t go out of their way to advertise. Your complaints alone don’t hold much legal weight, but a piece of paper from the Federal Trade Commission (FTC) absolutely does.

By visiting IdentityTheft.gov, you can fill out an official Identity Theft Report (sometimes called an Affidavit). Think of this document as your legal Golden Ticket. It proves to the government, the credit bureaus, and the banks that you are formally swearing—under penalty of perjury—that you are a victim.

Why is this FTC report so crucial? Because of a little piece of legislation called the Fair Credit Reporting Act (FCRA), specifically Section 605B. This is your legal power move.

Most people think it takes months of begging to get fraudulent charges removed. But under Section 605B, once you provide the credit bureaus with your official FTC Identity Theft Report and proper identification, they are legally required to block that fraudulent information from your credit report within four business days. You don’t have to wait for an eight-week investigation; the law says they have to hide the bad data right away.

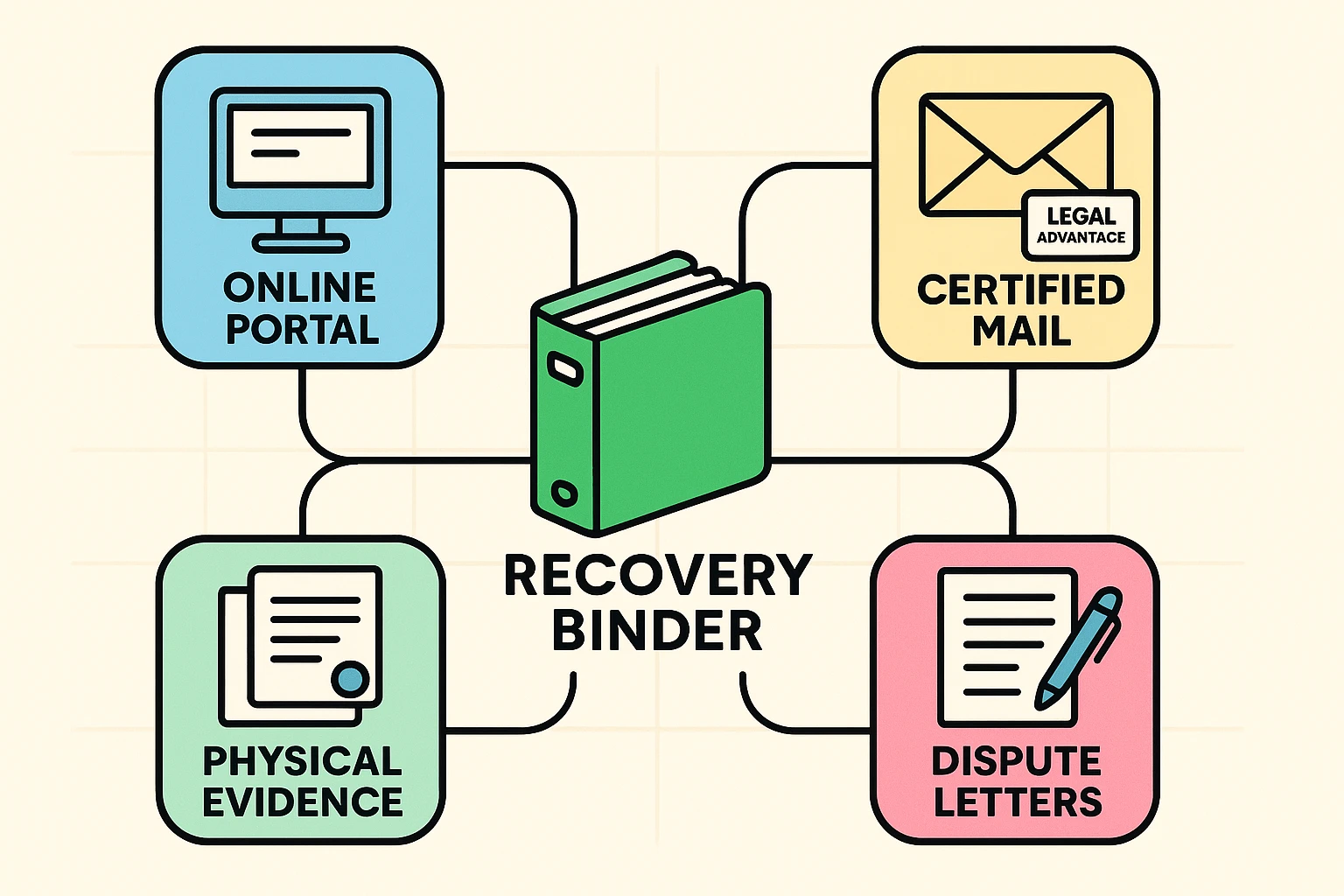

We live in a digital world, and the credit bureaus will try very hard to push you into using their online dispute portals. They will make it look easy, with big shiny buttons and simple drop-down menus. Do not fall for it.

When you use an online portal, you are forced to fit your complex legal problem into a tiny multiple-choice box. Worse, by clicking “submit,” you often unknowingly agree to forced arbitration, signing away your right to sue them if they mess up.

Instead, we recommend the “Identity Theft Recovery Binder” method. You are going to act like a lawyer building a case, and you are going to use the U.S. Postal Service. When you dispute an account, type a clear letter, attach a copy of your FTC report, and mail it via Certified Mail with a Return Receipt. This creates an undeniable paper trail that proves exactly when they received your dispute, starting the legal clock on their response time.

When we hear “identity theft,” we usually picture stolen credit cards. But for seniors, one of the fastest-growing crimes is medical identity theft. This happens when a scammer uses your Medicare or health insurance number to get treatments, surgeries, or prescription drugs.

This is especially dangerous because it doesn’t just mess up your credit score; it messes up your medical records. If a scammer has a different blood type or is allergic to penicillin, that false information can end up in your file.

If you get a bill from a clinic you’ve never heard of, don’t just toss it in the recycling bin. Take a moment to check their website to see if they are a real facility, then call your insurance provider immediately. You will need to dispute these charges just like you would a fraudulent credit card, keeping meticulous records of who you spoke to and when.

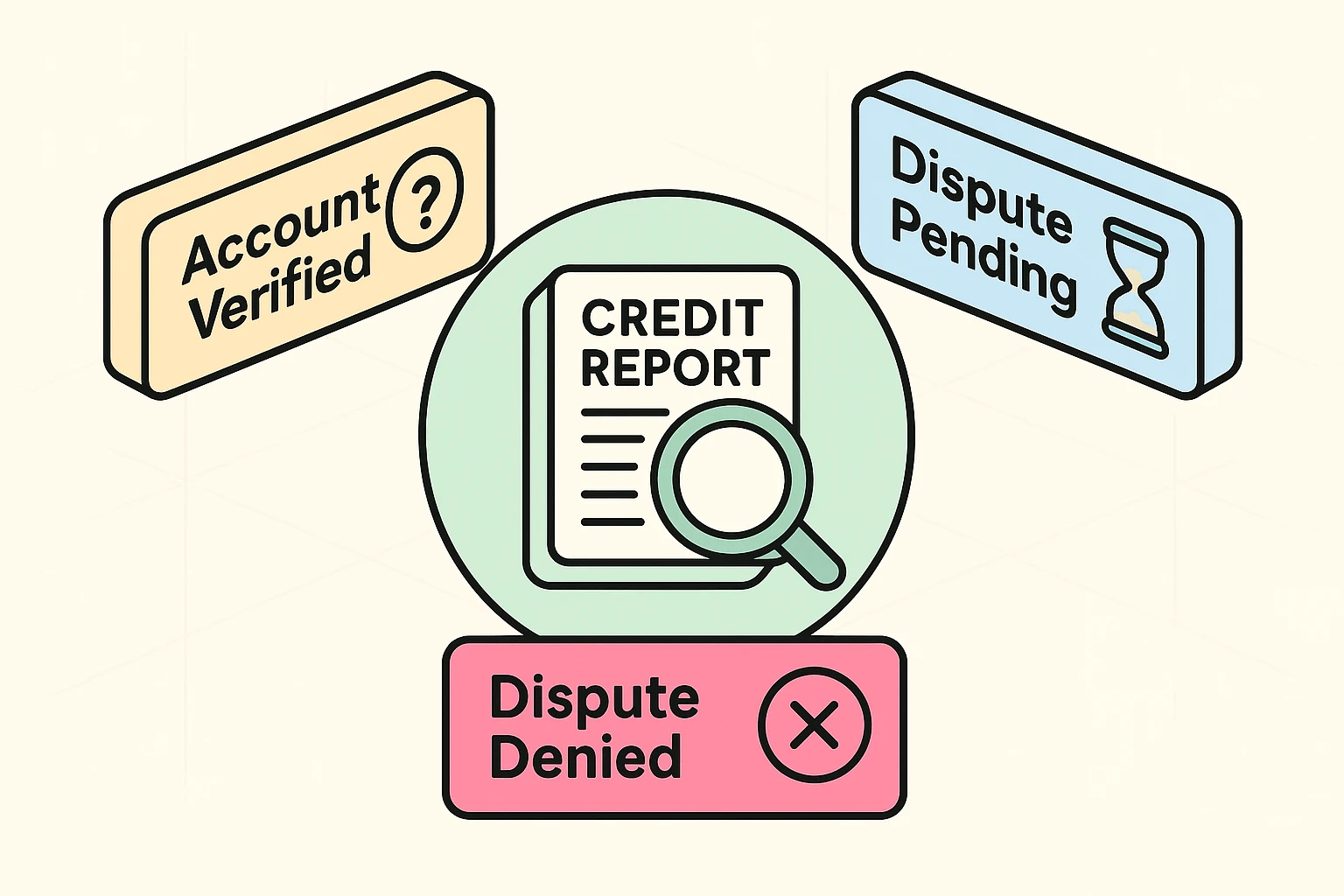

Eventually, you will receive a response from the credit bureaus. Sometimes it’s good news, but often, you’ll hit what we call the “Verified Wall.” You’ll get a letter claiming your dispute was rejected because the account was “verified.”

To a normal human, “verified” means someone did a thorough investigation and uncovered the truth. In bureau-speak, “verified” usually just means their computer sent an automated code to the bank’s computer, and the bank’s computer replied, “Yep, that’s the name on the account.” It is incredibly frustrating, like arguing with a brick wall that only speaks in barcodes.

Do not let this discourage you. The bureau is acting as a gatekeeper, and gatekeepers hate persistence.

If your dispute is rejected, it’s time for the Re-Dispute. You send another Certified Letter, but this time you ask for their “Method of Verification.” By law, they have to tell you exactly how they verified the account, including the name and number of the person they spoke to. Usually, they can’t do this, because no human actually looked at it.

If they still refuse to budge, you have the legal right to add a 100-word “Consumer Statement” to your credit report. This allows you to attach a permanent note to your file stating that the account is fraudulent and currently under dispute, warning any future lenders that the information is bogus.

A furnisher is the company that provided the loan or credit card (like Chase or Home Depot). A credit bureau (like Experian) is the company that collects that information and builds your credit score. You often have to dispute the fraud with both of them to get it completely cleared.

In most cases, absolutely not. By using the FTC Identity Theft Report and sending disputes via Certified Mail, you are using the exact same legal tools a lawyer would use. Save your money for something fun, like extra guacamole or spoiling your grandkids.

While the 4-day block rule (Section 605B) works quickly to hide the information, fully cleaning a badly mangled credit report can take anywhere from three to six months. Treat it like a marathon, not a sprint.

Recovering from identity theft is a chore, but it is entirely manageable when you know your rights and refuse to back down. Remember, you hold the power of the FTC Affidavit and the U.S. Postal Service in your hands.

Once your credit report is scrubbed clean, the best offense is a good defense. Take some time to review your online security habits, ensure your software is up to date, and learn the warning signs of modern phishing scams. Technology should work for you, not against you—and with a little bit of knowledge, you can keep the scammers right where they belong: out of your wallet.