Newsletter Subscribe

Enter your email address below and subscribe to our newsletter

Remember the good old days when buying something involved a physical transaction? You handed a cashier a slightly crumpled twenty-dollar bill, they handed you a bag of groceries, and that was the end of the relationship. You didn’t have to worry that the grocery store would quietly reach into your wallet three weeks later and take another twenty dollars because you forgot to “unsubscribe” from the concept of bananas.

Welcome to the modern era of “Subscription Creep.” Today, everything is a subscription. You want to watch a movie? Subscription. You want to listen to music? Subscription. You want a razor to shave your face? Believe it or not, subscription.

It’s easy to sign up for a “free trial” of a streaming service to watch one show, or agree to a monthly vitamin delivery because you swore this was the year you’d get healthy. But then life happens. You forget. And suddenly, your credit card statement looks like a CVS receipt that goes on forever, filled with tiny charges for things you don’t use, don’t want, or don’t even remember existing.

You aren’t losing your memory; you’re just navigating a digital minefield designed to make you pay and forget. Today, we’re going to put on our detective hats (and maybe our reading glasses) to hunt down these “ghost” charges and put that money back where it belongs: in your pocket.

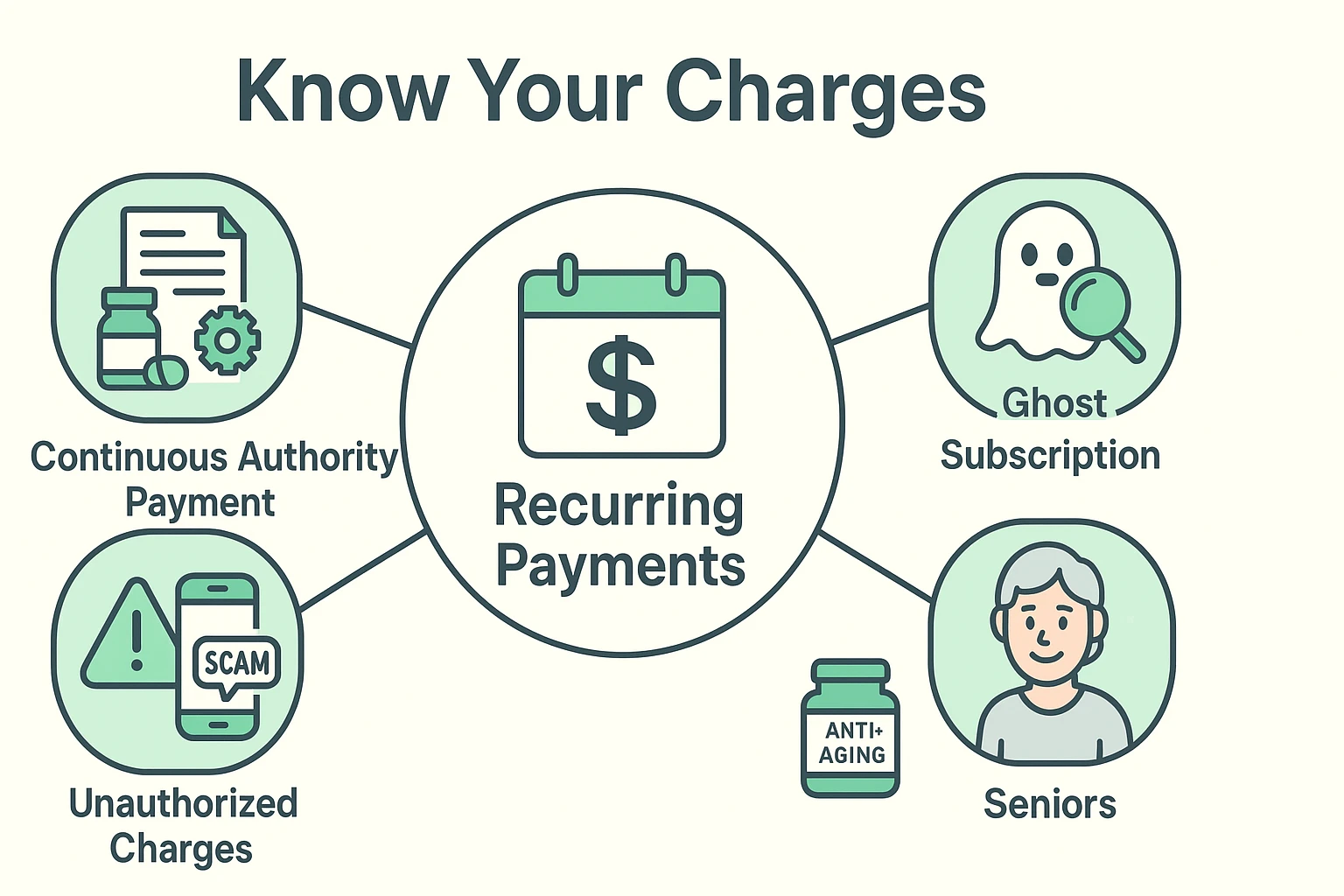

Before we start slashing bills, we need to know what we are looking for. A Recurring Charge is any payment that happens automatically on a schedule—usually monthly or annually. These are great for your electric bill, but terrible for that “Fruit of the Month” club you lost interest in back in 2018.

The real troublemakers are what we call Ghost Subscriptions. These are charges for services you:

These charges rely on the “Gym Membership Model”—they hope you feel too guilty or too confused to cancel. But here at Senior Tech Cafe, we don’t do guilt. We do action.

Grab your most recent bank and credit card statements. If they are digital, open them on your largest screen. If they are paper, grab a highlighter and a strong cup of coffee. We are going on a treasure hunt, but instead of gold, we are finding your own money.

Scan your statement. Skip the big obvious things like the supermarket or the gas station. You are looking for the little guys. Scammers and shady subscription services know that if they charge you $500, you’ll notice immediately. But if they charge you $9.99 or $14.95? Your eyes might glide right over it.

Look for names you don’t recognize. Often, the name on the bill is different from the product. You might have bought “Super-Glow Face Cream,” but the charge shows up as “SG Global Marketing LLC.”

When you find a charge that makes you say, “What in the blue blazes is this?”, don’t panic. It happens to the best of us.

Sometimes the charge is legitimate but obscured by a payment processor. For example, you might see a generic charge if you used a digital wallet or a service like paze shopping, which consolidates your cards for easier checkout.

If the name is totally unfamiliar, type the text exactly as it appears on your statement into Google, followed by the word “charge.” For example: “TechSupp Svcs 800 charge.” You will likely find forums of other people asking the same question, which will tell you exactly what the service is.

This is the most critical step. There is a common misconception that if you just tell your bank to stop paying, the problem goes away. This is false.

Think of it this way: If you sign a lease for an apartment and then just stop writing rent checks, you haven’t canceled your lease—you’ve just become a delinquent tenant. The landlord (or Netflix) still thinks you owe them money.

You must contact the merchant first. Look for a “Cancel Subscription” link on their website, or call their customer service number. Keep a record of the cancellation confirmation number. You might need it later to prove you broke up with them.

If the merchant refuses to cancel, or if you can’t get hold of them (because their phone number leads to a fax machine in a basement somewhere), then it is time to call your bank or credit card issuer.

You have two superpowers here:

When it comes to fighting these recurring charges, not all plastic is created equal. Using a debit card for subscriptions is like riding a motorcycle without a helmet—it’s thrilling until something goes wrong.

When a shady subscription hits your Debit Card, the money is gone instantly from your checking account. It’s real money. You might need that money for groceries or utilities. Getting it back can take weeks while the bank investigates.

When a charge hits your Credit Card, no actual money has left your pocket yet. You are spending the bank’s money. If you dispute a charge, you simply don’t pay that portion of the bill while the bank sorts it out. The law (specifically the Fair Credit Billing Act) offers much stronger liability protection for credit cards than for debit cards.

Be especially vigilant for these “classic” subscription traps that often target older adults:

It used to be just “annoying,” but the government is cracking down. The Federal Trade Commission (FTC) is proposing a “Click-to-Cancel” rule. The idea is simple: if it was easy to sign up, it must be equally easy to cancel. Until that becomes strictly enforced everywhere, however, some companies will still make you jump through hoops.

This sounds like something a general would order in a war movie, but it’s actually a banking term. It means you gave a merchant permission to take money from your card whenever they want, for varying amounts. This is different from a “Direct Debit,” which has stricter guarantees. Continuous Authority payments (often used for subscriptions) are harder to block, which is why monitoring your statement is vital.

This is the nuclear option, but it doesn’t always work! Many credit card companies offer “updater services.” If you get a new card number, they automatically send the new number to your subscription services so your Netflix doesn’t get cut off. Convenience for you, but also convenience for the scammers. You must cancel the service directly with the merchant to be safe.

Generally, for credit cards, you have 60 days from the time the statement was sent to you to dispute a billing error. This is why opening your mail (or checking the app) every month is so important. If you find a charge from three years ago, you can stop future payments, but you likely won’t get that old money back.

Technology is supposed to make our lives easier, not drain our bank accounts $12.99 at a time. By taking fifteen minutes once a month to review your statement, you aren’t just saving money; you’re taking a stand against the “subscription creep” culture.

So, pour yourself another cup of coffee, grab that highlighter, and show those ghost charges who is boss. And if you find a subscription for a “Jelly of the Month” club you don’t remember joining… well, maybe wait to see what flavor arrives before you cancel.